Save Tens of Thousands by Employing Your Spouse!

Most dentists employ their spouse so they can contribute to the practice retirement plan, but many more choose not to or think that because their spouse is employed elsewhere, the benefits are null and void. However, this isn’t the case! There are hidden tax savings available to all practice owners for employing their spouse. You simply need a valid business reason to have them on payroll. One of my favorite questions to ask the audience at our seminars is, “Does your spouse provide you with any practice advice, whether it be solicited or unsolicited?” We always get a good chuckle to kick the day off. Unfortunately, if your spouse is not on your payroll, you’re leaving thousands on the table each year!

Benefit #1: Increased Retirement Plan Contributions

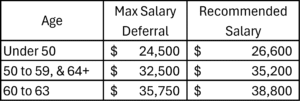

If your spouse isn’t employed elsewhere, employing them at your practice and making the maximum tax-deductible salary deferral into your 401(k) profit sharing plan can save you up to $10,000 or more in federal and state income taxes. We recommend setting their salary to the lowest possible amount to maximize the salary deferral and minimize payroll taxes. Overpaying your spouse is another mistake you want to avoid. If your spouse is on the payroll for $50,000, instead of the $26,600 required to maximize the 401(k) salary deferral for spouses under age 50, you’re overpaying payroll taxes by more than $3,500 annually! We recommend setting the appropriate salary based on the following table:

Benefit #2: Lower Staff Costs

Many dentists choose to not employ their spouse since their spouse works elsewhere and already maximizes their 401(k) salary deferral, making additional retirement plan contributions an afterthought. While we agree with having your spouse maximize their salary deferral at their employer since this will add thousands in matching contributions from their employer, this doesn’t mean your retirement plan has no benefit of adding your spouse! Simply adding your spouse to the plan can help reduce staff costs of profit sharing contributions.

If your spouse is employed elsewhere, we recommend having him or her on payroll for $250 per month and making them eligible for the plan. To make him or her eligible, you will either need to mark them as having previously worked 1,000 hours if they qualify or waive eligibility for all currently employed staff members. However, be wary waiving eligibility if you have part time staffers that aren’t currently in the plan, as you may inadvertently cost yourself more.

Benefit #3: Increased Tax Deductions

Can you write off the cost of your spouse travelling with you? No! Unless of course, your spouse is an employee of the business as well! Even if your spouse is employed elsewhere, we recommend a minimum salary of $250 per month to qualify for tax deductible perks, such as tax deductible travel and meals. Make them even happier by joining our seminar in Napa, where you’ll learn how to pay less tax in the morning while sipping wine in the afternoon.

Make sure to check out our previous blog posts, Is Your Vacation a Tax Deduction? and Does Your Night Out Qualify as a Tax Deduction?, for more details on how to maximize your perks as an owner.

Benefit #4: Build Social Security Benefits

To be eligible for social security benefits, you need at least 40 credits, or 10 years of work history. Even a spouse with minimal credits will be eligible for spousal benefits, providing a great return on investment for paying minimal social security taxes. Credits are earned based on time as well as minimum earnings, but any spouse earning enough wages to maximize their 401(k) salary deferral will become eligible for social security, often earning total lifetime benefits of more than $500,000, even if salaries are kept minimal.

Benefit #5: Increased Vehicle Deductions

Did you read our recent blog post, Can You Deduct 100% of the Cost of a New Vehicle?, and decide you don’t qualify? There could be a work around. If your spouse can qualify for more than 50% business use since he or she doesn’t have a regular commute, you can potentially write off a vehicle through the business for them. Common duties include making deposits at the bank, picking up supplies, lab drop offs, mail, etc. Since your spouse does not have a regular commute, the 50% business use can be achievable in the case of long commutes for the dentist.

Make sure to talk with an expert CPA who provides advice tailored to you prior to implementing this strategy!

Listen to Tyler and Wes jump into this topic more in this short explainer video, or listen to the audio version on Spotify or Apple Podcasts.

Want to stay up to date on all tax, practice, and financial strategies for dentists?

Want to ensure you’re utilizing all possible tax saving strategies correctly? Request a call with our Tax and Business Planning team!